Most people in the UK will need to borrow money eventually. Whether it’s for a first car or a family home, your credit score sits at the heart of the process. It’s a record of your past financial behaviour that lenders use to predict how you’ll act in the future.

It’s worth pointing out that you’ll find different debts carry different weights on your report. A credit card balance doesn’t look the same to a bank as a mortgage or a car finance agreement. Knowing these details will help you manage your financial health effectively, so find out how it all works below.

How Credit Cards and Revolving Debt Change Scores

Credit cards are known as revolving credit because you don’t have a fixed end date for the debt. You can spend up to a limit, pay it off, and then spend it again. This borrowing is a major factor in your credit score because it shows how you handle available funds. Lenders want to see you’re responsible enough not to max out your cards.

It’s a good idea to keep your credit utilisation ratio low. This is the percentage of your total limit that you’re actually using. If you have a three thousand pound limit and spend two thousand, your ratio is high. This can signal to lenders that you’re relying too much on credit to get by.

Secured Car Finance and Long-Term Stability

Car finance is a unique category because it’s often secured against the vehicle itself. This is a significant distinction from a standard personal loan where the money is yours to spend as you wish. When you opt for a hire purchase loan, you’re essentially entering an agreement where the car acts as collateral. This means the finance company owns the car until the final payment is made.

From a credit perspective, this shows lenders you can manage an asset-backed debt. They’ll see you’re committed to a regular payment schedule to keep the vehicle you use daily. It’s often viewed as a stable form of debt compared to a credit card. You’ll see a positive impact on your score if you maintain these payments over the long term.

Why Mortgages Act as the Ultimate Credit Test

A mortgage is usually the largest debt anyone will ever take on. Because the sums are high, the impact on your credit score is substantial. When you first apply, you’ll see a small dip in your score due to the hard search conducted by the bank. This is normal and happens with almost any loan application.

Consistent mortgage payments are gold dust for your credit file. They show you can handle a massive financial commitment over decades. While other small loans come and go, the mortgage remains a steady anchor on your report. If you ever want to borrow for other things, a clean mortgage history will make you look like a safe bet.

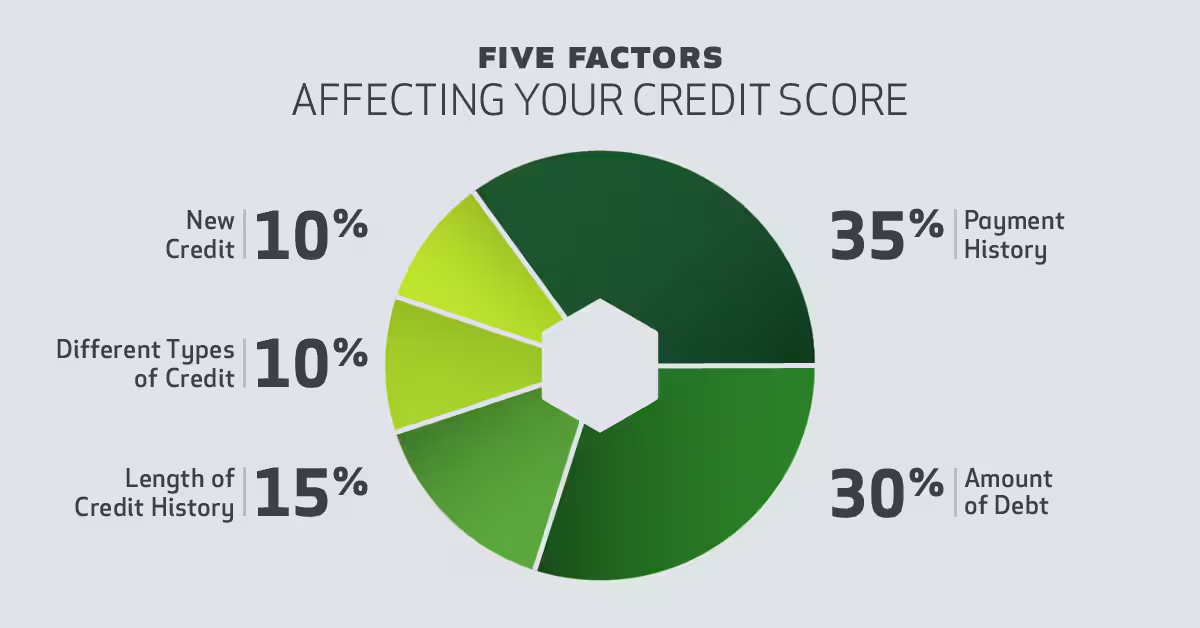

Specific Metrics That Shape Your Profile

Lenders look at several specific factors when they scan your credit file:

- Your total level of outstanding debt across all accounts.

- The length of your credit history and the age of your oldest account.

- Whether you’ve missed any payments on your agreements.

- The number of hard searches conducted on your file recently.

- Your current credit utilisation ratio on revolving accounts.

Each of these points helps a lender decide if they’ll give you a competitive interest rate. If you have a mix of credit types, like a credit card and a car loan, it can help your score. It shows you’re capable of managing different rules and repayment structures.

To Wrap Up

Managing your credit score is more about showing you can handle different types of borrowing without getting into trouble instead of avoiding debt entirely. Whether you’re using a credit card or paying off a car, consistency is what matters most.

You’ll find that your score grows naturally as you prove you’re a reliable borrower. Keep a regular eye on your report and you’ll be in a great position whenever you next need to apply for finance.